How To Understand The Basics Of The Cash Flow Statement

I have good news for you – it is not too difficult to understand the basics of the Cash Flow Statement – even if you don’t consider yourself a “numbers person”!

Although many entrepreneurs cringe and may even feel a bit of trepidation when they hear the words financial statements, in reality, once you understand a couple of basic concepts, they are quite straightforward.

Here we will focus on understanding the basics of the Cash Flow Statement.

First, let’s review the basics of financial statements in general.

There are three main financial statements with which you need to be concerned as a startup or small company entrepreneur. Those financial statements are:

The Income Statement (a/k/a “Profit And Loss Statement,” or simply “P&L”)

The Income Statement gives you a picture of your Revenues and Expenses over a period of time, most frequently monthly, quarterly or annually, but it can be over any period of time. When you subtract your Expenses from your Revenues, you get your Profit (or “Income,” “Operating Income,” or “Net Income,” depending which expenses you include in the calculation).

The Balance Sheet

The Balance Sheet gives you a snapshot at a point in time (not over a period of time) of your Assets, Liabilities, and Equity. Assets minus Liabilities equal Equity (or “Net Worth”).

The Cash Flow Statement (a/k/a “Statement Of Cash Flows”)

The Cash Flow Statement, as calculated in this article, pulls information from both the Income Statement and the Balance Sheet, to give you a picture of changes in your cash position over a period of time.

The Cash Flow Statement begins with the cash balance at the beginning of the period you are looking at, and ends with the cash balance at the end of the period you are looking at.

Three Parts Of The Cash Flow Statement

The Cash Flow Statement has three parts that you must consider in order to calculate the change in cash balance during the period in question. Those parts are:

Cash Flow From Operations (CFO)

This part starts with the Net Income (from the Income Statement) generated by your business, then adjusts that Net Income up or down for the non-cash effects of operating income. We’ll touch on this in more detail in the example below.

Cash Flow From Investing Activities (CFI)

This part makes adjustments to the cash balance based on cash generated or used by investing activities. Such activities could include the sale of long-term assets, capital expenditures on equipment, and the sale or purchase of other assets, among other investing activities.

Cash Flow From Financing (CFF)

This final part of the cash flow statement accounts for changes in the cash balance that result from financing activities, such as taking out or paying off loans, selling stock, and paying dividends.

Here is a very basic example to illustrate the three sections of the Cash Flow Statement and walk you through some of the calculations you will have to consider in creating your own Statement of Cash Flows.

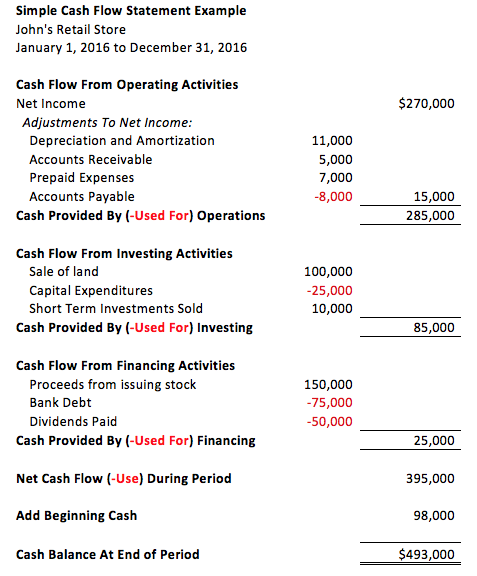

This sample Cash Flow Statement of John’s Retail Store showing cash flows for the period January 1, 2016 to December 31, 2016 will allow us to talk through some of the concepts described above.

The Cash Flow Statement starts with Cash Flow From Operations (CFO), with the first element of CFO being Net Income.

The Net Income figure would be taken from John’s Retail Store’s Income Statement for the same period of time.

The Net Income is then adjusted for non-cash items that occurred during the same period. The basic concept here is that whatever is shown on the Income Statement as Net Income results from subtracting Expenses from Revenues for the period. Usually though, not all the Revenues are received in cash, and not all the Expenses are paid in cash.

So, in order to understand the cash impact of these Revenue and Expense transactions during the period, you need to look at the change in relevant Balance Sheet accounts during the same period. For example, you’ll see in the illustration above that there was a change in Accounts Receivable (A/R) during the period that had a net positive effect on cash of $5,000. In the world of accrual accounting, this would mean that A/R (on the Balance Sheet) went down $5,000 during the period.

I realize that this may be a bit confusing. Think about the opposite example, which may help to clarify it in your mind. That is, if A/R went up $5,000 during the period, that would have a net negative effect on Cash Flow of $5,000 during the same period. Why is that? Remember the adjustment here is to Net Income. If $5,000 of Revenues came in, but were not collected, that would be a $5,000 increase in A/R relative to the Net Income that was reported during the same period. In other words, $5,000 that is part of the Net Income is not part of cash during that same period, so it would need to be netted out (subtracted) in the CFO section on the Cash Flow Statement.

Let’s take another example in the Cash Flow From Operations section on John’s Retail Store’s sample Cash Flow Statement. You can see that the change in Accounts Payable (A/P) had a negative $8,000 effect on cash flows. What would this mean? Similar to above, but actually opposite, since it’s A/P instead of A/R, if A/P went up on the Balance Sheet, it would have a positive effect on cash flow for the period. If, on the other hand, as occurred in the case of the John’s Retail example above, A/P went down, it would be a use of cash during the period. In this case, A/P on John’s balance sheet was paid down, using cash, by $8,000 during the period.

I won’t go into details here on the Depreciation and Prepaid Expenses entries in the sample Cash Flow Statement above, but if you have questions, don’t hesitate to ask.

Let’s move on to Cash Flow From Investing Activities.

This section is quite straightforward, as it doesn’t involve adjustments to the Net Income. Rather, Cash Flow From Investing Activities describes changes in cash during the period that result from, you guessed it, “investing activities”. In the case of the Cash Flow Statement, these investing activities include such things as buying and selling assets and investments, including capital expenditures on equipment needed to run the business. In the John’s Retail example above, investing activities has a net positive effect on cash of $85,000 during the period.

Finally, let’s talk about the third section of the Cash Flow Statement, which is Cash Flow From Financing Activities. As with the other sections, these flows can be positive or negative, depending on whether you are receiving the proceeds of financing activities, or paying off financing during the period. As you can see above financing activities in this context include such things as debt (loans), stock issuance, and payment of dividends. In the case of John’s Retail during the period, investing activities had a net positive effect on cash of $25,000.

The final step on the Cash Flow Statement involves adding to, or subtracting from, as the case may be, the net result of the above three sections, the beginning cash balance for the period, to arrive at the ending cash balance for the period.

It’s pretty straightforward:

Beginning Cash Balance

Plus: Net Effect of CFO, CFI, and CFF during the period

Equals Ending Cash Balance.

As you can see from the above example, although the calculations are slightly nuanced, given the peculiarities of Accrual Accounting (i.e. not all transactions are on a cash basis, so adjustments need to be made to the Net Income), the overall idea of the Cash Flow Statement is not too complicated.

As with the other two main financial statements, the Income Statement and Balance Sheet, it’s important that you understand the basics of the Cash Flow Statement, as it will help you run your business better and it will help you more confidently manage financial conversations with important constituencies, such as employees, accountants, lenders, and other potential sources of financing or liquidity.

And, as the saying goes, “cash is king”!